The purchase of a house through the affordable housing program is an exciting milestone; however, for many applicants, it can be a source of dismay when the funds don’t arrive in time. If you’ve asked, “Where is my PMAY subsidy?” It’s not a problem.

This guide will explain the reasons why your subsidy could be delayed, the best way to follow the process step-by-step, and the steps you should take to address the issue, so that you will be able to determine how the Pradhan Mantri Awas Yojana (PMAY) actually functions in 2026.

What Is PMAY Subsidy and How Does It Work?

PMAY subsidy PMAY loan subsidy is available as part of the Credit Linked Subsidy Scheme (CLSS) that reduces the interest on your home loan. Instead of receiving cash directly from an account in your banking institution, the benefit goes to:

- Credit on your mortgage home account.

- Adjusted to the amount you pay for your main account

- Processing is done by your lending institution or a housing finance company

If, for instance, you’re eligible for the Rs2.67 thousand subsidy, the amount of your loan will decrease accordingly, thereby reducing your EMI or the term.

Why Is Your PMAY Subsidy Delayed in 2026?

There’s no single reason for delays. delays are usually caused by several elements. Here are the most frequently-cited ones:

1. Bank-Level Processing Delays

Your bank plays a key function in:

- Verifying documents

- Sending in your applications into the PMAY portal

- Coordination with other agencies

Even a minor backlog can delay your subsidy.

2. Incomplete or Incorrect Documentation

Errors can be found in:

- Aadhaar details

- Income documentation

- Documents about property

could result in rejection or require reprocessing.

3. Pending Verification by Nodal Agencies

Your application is scrutinized by central nodal agencies such as:

- National Housing Bank (NHB)

- Housing and Urban Development Corporation (HUDCO)

If verification is not completed your subsidy will not be granted.

4. Property Eligibility Issues

Not all properties qualify. Delays could occur in the event of:

- The property’s carpeting exceeds the permitted carpet area.

- The developer hasn’t registered the project correctly.

- The project isn’t in compliance with the requirements of PMAY

5. Subsidy Not Yet Released by Government

After approval, the funds are distributed in groups. This means that often:

- Your application has been accepted

- But the funds are awaiting release.

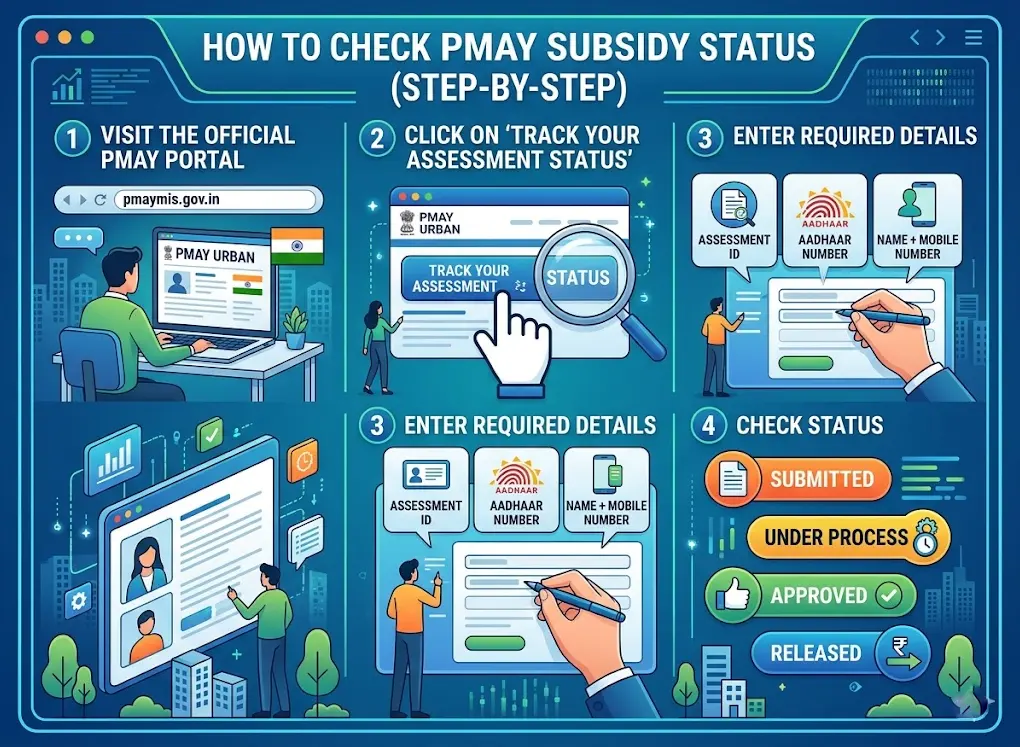

How to Check PMAY Subsidy Status (Step-by-Step)

Tracking your subsidy status is easier than most people think. Follow these steps:

Step 1: Visit the Official PMAY Portal

Go to the official website of PMAY Urban

Step 2: Click on “Track Your Assessment Status”

This option is available on the home page.

Step 3: Enter Required Details

You can track using:

- Assessment ID

- Aadhaar number

- Name + mobile number

Step 4: Check Status

- Submitted – Application filed

- Under Process – Verification ongoing

- Approved – Subsidy sanctioned

- Released Subsidy to your lender

How to Track PMAY Subsidy Through Your Bank

Because the money is transferred to your account for loans the banking institution is your most trustworthy source of information.

What can you do?

- Speak to your loan advisor

- Request your CLSS status update

- Check if the grant is being acknowledged internally

Tips: Even if the government has announced subsidies, they could take a while until the institution can include the subsidy on your statement of loans.

What to Do If Your PMAY Subsidy Is Stuck

In case your situation hasn’t been changed over the last few months, don’t sit around and wait. do something about it.

1. Contact Your Bank

Always take this as your first step. Ask:

- Did my application get uploaded?

- Is it endorsed by the agency that regulates nodal?

- Is there a document issue?

2. Check for Application Errors

Verify:

- Aadhaar linking

- Category of income (EWS/LIG/MIG)

- Information about the property

Even minor mismatches can lead to delays.

3. Raise a Complaint on PMAY Portal

You can make a complaint directly on the PMAY site.

4. Contact Nodal Agencies

If your bank isn’t responding, you can escalate the issue to:

- NHB

- HUDCO

Include your application ID and the details of your loan.

5. Use CPGRAMS for Escalation

You can appeal to the Centralized Public Grievance Redress and Monitoring System (CPGRAMS) to get speedier resolution.

How Long Does It Take to Receive PMAY Subsidy?

There’s no definitive timeframe, but generally:

- 3 – 6 Months after the date of the loan payment

- It can be extended up to nine to twelve months in certain instances

A year-long delay can signify:

- Issues with the application

- Bank processing delays

- Pending approvals.

Common Mistakes That Delay Your PMAY Subsidy

Beware of these when trying to apply or waiting for approval:

- Applying to the wrong income category

- Not linking Aadhaar properly

- Selecting a property that is not approved

- Do not follow up with your lender

- Assuming that the subsidy can be directly credited to your bank account

Pro Tips to Speed Up Your PMAY Subsidy

- Beware of these when trying to apply or waiting for approval:

- Applying to the wrong income category

- Not linking Aadhaar properly

- Selecting a property that is not approved

- Do not follow up with your lender

- Assuming that the subsidy can be directly credited to your bank account.

Frequently Asked Questions

PMAY Subsidy is a federal benefit under the Credit-Linked Subsidy Scheme (CLSS) that reduces the burden of your home loan by reducing the principal and thereby shortening the EMI or loan term.

You can track your progress by logging onto the PMAY official portal, clicking “Track Your Assessment Status,” and then entering your Aadhaar code, application ID, or mobile number registered with the PMAY.

The delay in your subsidy could be due to bank processing issues, insufficient documents, pending approval from nodal agencies, or concerns about property eligibility.

In general, the process takes 3 to 6 months after the loan’s disbursement. However, in certain cases, it can take 9 to 12 months, depending on the approval and verification timelines.

The subsidy is not credited into your savings accounts. It is transferred directly to the mortgage account and then applied to the principal.

First, contact your lender to verify the status of your application, check for any errors in the documentation, and file a complaint through the PMAY portal, should you need to.

Yes, applications are denied for reasons such as:

- Documents that are incorrect or incomplete.

- Ineligible income class.

- Property that is not in compliance with the PMAY guidelines.

You can verify your status online or verify your bank. If you are approved, your status will be “sanctioned” or “released.”

Your lender handles the application process and is then confirmed by central nodal authorities such as NHB or HUDCO before the subsidy is made available.

Write Your Comment